FTX Trilogy, Part 2: Speedrun

Access to new, never before shared data illuminates a crypto behemoth.

Editor’s note: this trilogy was written in August 2021, fifteen months before FTX’s subsequent meltdown. We have kept it up to show our thinking at the time, and the view of the broader market. We reflected on the fallout and what can be learned in a coda to the trilogy, “The Casino and the Genie.”

You can find Part One and Part Three here.

MrCheeze had a bad July.

A year earlier, the gamer had made a bet: no one would ever finish The Legend of Zelda: Ocarina of Time in less than 7 minutes. It just wasn’t possible.

Savestate, another gamer, took up the gauntlet. It would take a flawless performance to succeed, he knew — no wasted button presses, or flubbed movements. In the end, he triumphed with just fractions of a second to spare. On July 22, Savestate completed Zelda in 6:59.767.

Why would anyone do this?

Savestate and MrCheeze are “speedrunners,” — players that aim to complete games as rapidly as possible, often in the hopes of setting a new record. People have speedran all manner of games including Super Mario 64 (1 hour 38 minutes 21 seconds), Sonic the Hedgehog (54 minutes 17 seconds), and Grand Theft Auto V (5 hours 49 minutes 8 seconds).

While the goal of speedrunning is, explicitly: go fast, it takes a lot more than that to be successful. As much as being fleet-fingered, speedrunning is about knowing what you can afford to ignore, to miss out on, and still win. The goal is not to reach the game’s conclusion with the protagonist’s coffers swollen and every sidequest finished, but simply to arrive.

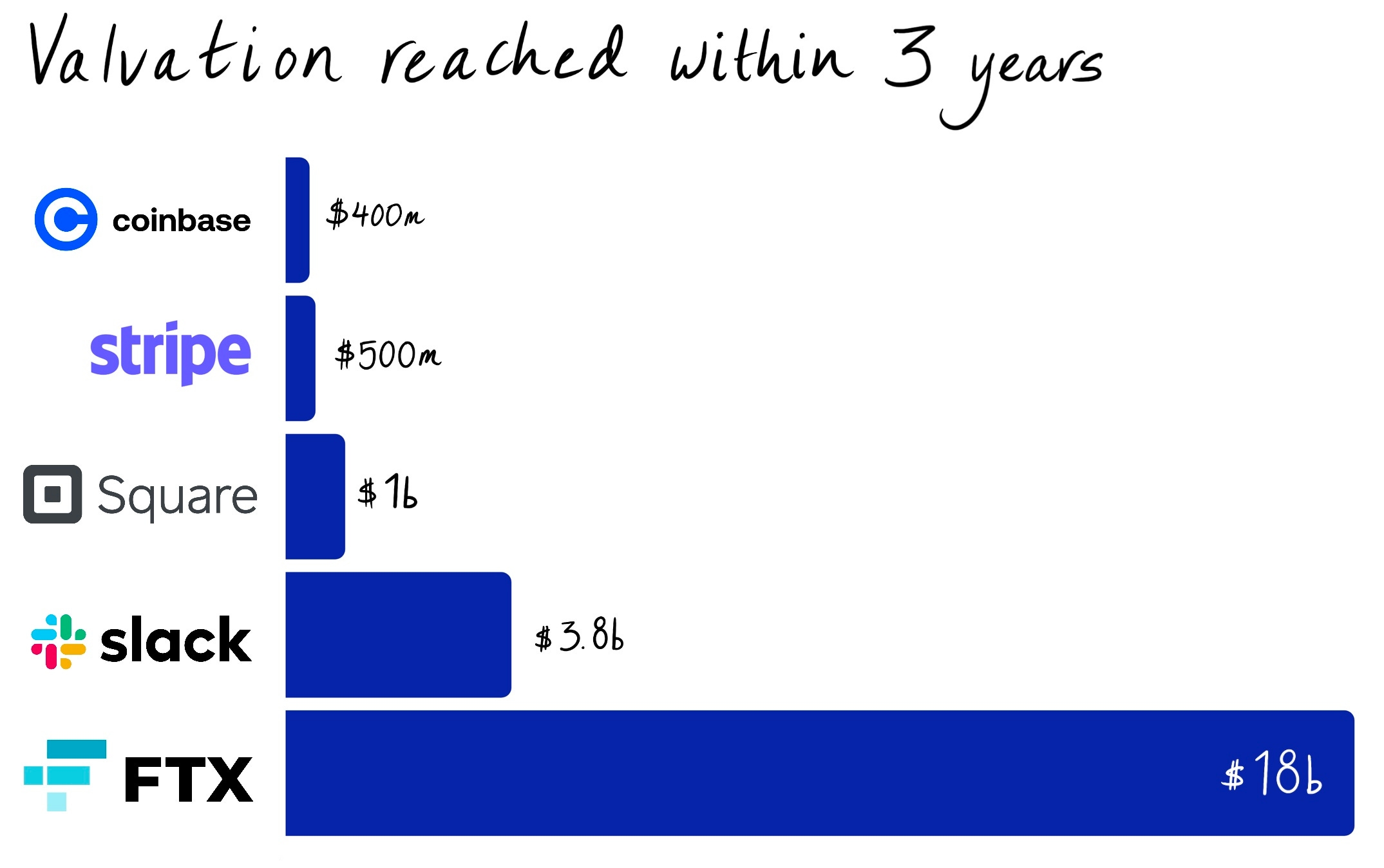

In both its strengths and deficits, FTX reads like a kind of speedrun. In just 26 months, the company has secured an $18 billion valuation, becoming one of the most popular crypto exchanges in the world. That makes it one of the fastest companies ever on a value accrual basis, besting legendary businesses like Coinbase, Stripe, Square, and Slack.

But like every speedrunner, to achieve that velocity, FTX has had to make concessions. In particular, the exchange has played fast and loose with regulation, shrugged off accusations of conflicts of interest, and largely ignored retail traders.

Those lapses may take a toll. Believers will note that the company seems to have the capital, connections, and will to resolve its most significant problems. Of course, only time will tell how effective FTX is in filling the gaps.

Today, we’ll explore different dimensions of the FTX empire, with the help of never-before-seen data on the business. Our investigation will touch upon:

Early days. FTX’s fast start and near-instant product-market fit.

Product. How the company differentiated on reliability and creativity.

Customer base. Winning over serious traders from around the world.

Metrics. An inside look at FTX’s traction.

Competition. How FTX compares to Coinbase, Binance, BitMEX, and others.

Bear case. The ways FTX might implode.

Let’s get to it.